We are committed to sharing unbiased reviews. Some of the links on our site are from our partners who compensate us. Read our editorial guidelines and advertising disclosure.

Entrepreneurs Are Risking Personal Finances to Start Businesses

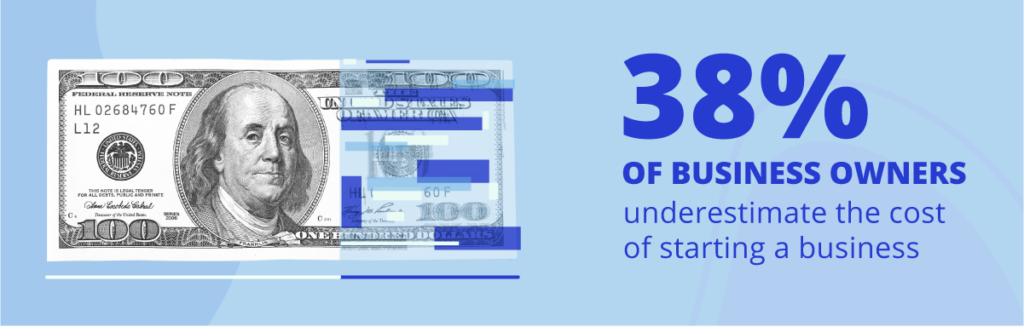

The initial financial challenges of starting a small business are substantial and often unpredictable. In fact, 38% of small-business owners report that they underestimated how much it would cost to start their business.

When hidden costs arise, many turn to outside funding—according to findings from our new survey of over 700 business owners, one in three entrepreneurs report that having access to personal loans and business credit cards is what helped them start their business.

Unfortunately for some businesses, credit can be a serious barrier to meeting the financial challenges of starting a business. A whopping 43% of business owners say their score isn’t high enough to qualify for traditional small-business lending.

Not having access to additional funds when problems arise can be fatal to small business hopes and dreams, especially when you consider that only 32% of business owners have an emergency fund in case their business doesn’t generate revenue.

Get Access to Our Research Reports

Provide your email to receive our reports on small-business and industry trends.

By signing up I agree to the Terms of Use and Privacy Policy.

The financing strategies of small-business owners

Financing is crucial during the early stages of opening a business. But that’s also when it’s hardest to secure a loan. Only 30% of business owners say they were able to qualify for a small-business loan in the first year of business, with 26% reporting that high interest rates kept them from applying.

When traditional methods fail, enterprising entrepreneurs must turn elsewhere for their cash. We asked small-business owners what they do when they need extra money, and this is what they said:

- I used my personal savings to start my business. (43%)

- I used a personal loan to fund my business. (33%)

- I received financial support from friends and family to start my business. (35%)

- I used my personal credit card to fund my business. (34%)

- I used a home equity loan to fund my business. (31%)

- I’m investing in crypto to fund my small business. (34%)

- I’m investing in traditional stocks to fund my business. (33%)

In addition to this list of creative strategies, one in three business owners are relying on income from another job to fund their business and have had to cut personal expenses in order to keep their business afloat.

Our findings show no shortage of hustle in the small-business financing strategy department. Unfortunately, the rush to get financing can have unintended consequences down the road.

The unfortunate reality of small business debt

Small-business owners have no shortage of determination when it comes to starting their own businesses. This, unfortunately, leads many to leverage their personal finances—putting themselves and their property at great risk.

According to the responses, 32% of small-business owners have had their personal finances affected by their business, and 31% are unsure how to keep business and personal finances separate. Small-business owners feel the difficult realities of leveraging personal finances everyday.

We gathered a few responses from entrepreneurs on how they’re utilizing their personal finances, and this is what they said:

- My credit utilization ratio is above 30% since I’m using my personal finances to fund my business. (29%)

- I’m not saving for retirement so that I can personally fund my business. (30%)

- I’ve tapped into my personal funds because of the pandemic to run my business. (28%)

- I’ve maxed out my business credit card before. (46%)

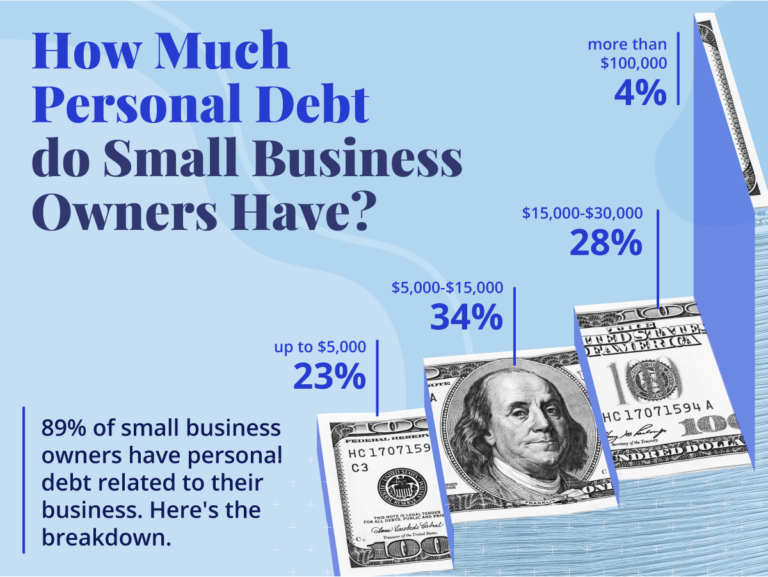

With so much small-business debt going around, it’s a miracle any small businesses are managing to stay debt free. Only 11% of small-business owners say that they have no personal debt related to their business.

For all other owners, the realities of debt are quite sobering:

- 23% report up to $5000 in personal debt related to their business.

- 34% report having $5000-15,000 in personal debt related to their business.

- 28% report up to $15,000-30,000 in personal debt related to their business.

- 4% report more than $100,000 in personal debt related to their business.

So much personal debt is dangerous to individuals’ livelihoods. And it’s all brought on by their inability to secure business financing.

The credit woes of entrepreneurs

Building credit is a top concern for small-business owners who want solid financing at a reasonable rate. In order to take charge of their credit, many small-business owners are considering credit monitoring. In fact, 31% say that free credit monitoring would help them build their credit score for business expenses.

Our experts here at Business.org have vetted a number of credit monitoring companies and were so impressed with one particular service that we decided to partner with them. If you want to take charge of your business credit, sign up for Credit Sesame today.

Being more deliberate and mindful about building credit is the key to accessing solid financing options now and in the future.

Methodology

We partnered with Pollfish to conduct an anonymous survey of 700 small-business owners with a +/- 2% margin of error with a confidence level of 95%. Business.org analyzed the results and compiled this report. To learn more about Pollfish and how it organically finds respondents, check out its methodology.

Recent Articles

EarthLink Business Internet Review 2026

Flexible, reliable business internet for small and growing teams. Flexible internet for small businesses Earthlink...

Fiber vs. Cable Business Internet for SMBs

How to choose a reliable internet connection with the uptime your small business needs For...

T-Mobile Business Internet Review 2026

Offers simple 5G business internet designed for small and growing businesses that want fast setup,...

Starlink Business internet review

Low-latency satellite internet for companies operating beyond the reach of traditional broadband. Best for Rural...