We are committed to sharing unbiased reviews. Some of the links on our site are from our partners who compensate us. Read our editorial guidelines and advertising disclosure.

Can Personal Loans Build Credit?: How Personal Loans Affect Your Credit Score

Quick facts

- 43% of small-business owners report that their credit wasn’t high enough to qualify for traditional small-business loans.

- 45% of small-business owners say they don’t understand the difference between a business credit score and personal credit score.

Credit scores can feel mysterious, thanks to secret algorithms and score fluctuations that seem random. But, as it turns out, you can predict how something will affect your credit score.

So if you’re wondering if a personal loan can improve your credit score, we’re happy to tell you that the answer is yes. Except, well, it’s a little more complicated than that. You might even see a dip in your score before you see a boost.

Don’t worry, though. We’ll break it all down for you. This guide will explain how a personal loan can change your credit score over time, why it has that effect, and what other things you can do to improve your credit.

How will a personal loan affect your personal credit score?

A personal loan (like any kind of installment loan) can help your credit score, but it can hurt too. In fact, your personal loan will probably do both.

We’ll get into exactly how that happens in just a moment. But for context, let’s first talk about how credit scores get calculated in the first place.

Does my personal loan show up on my credit report?

Yes, your personal loan will be on your credit report, and it will affect your credit score. In fact, even after you pay it off, your closed loan account will stay on your credit report for another seven years (give or take, depending on your credit bureau).

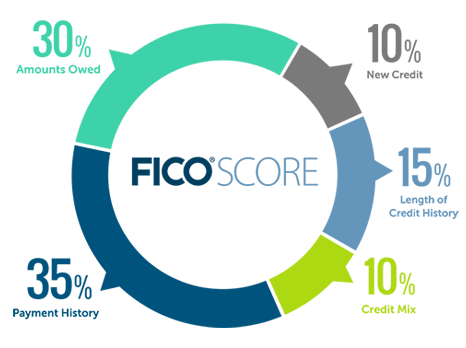

Credit score factors

To determine your credit score, a credit bureau considers several different factors. While all these factors matter, they don’t all get equal weight in your credit score. In other words, some factors matter more than others (as you can see in the graphic below).

Applying for a small-business loan soon?

Our free checklist can help you understand what lenders are looking for.

By signing up I agree to the Terms of Use.

Your payment history (worth 35% of your score) has the most weight. Have you paid your past credit back on time? Then you should have a good payment history. This includes payments on installment loans (like a personal loan or your mortgage) and payments on revolving credit (like credit cards). Better payment history will lead to a higher credit score.

The next most important factor is the amount owed (30%), which you can also think of as your current credit utilization ratio. You'll have a very high credit utilization ratio if you max out all your credit cards. But if you carry a smaller balance on each, you'll have a better ratio. So if you’re using 95% of the credit available to you, for example, you might end up with a lower credit score than if you’re using around 10%.

Next in line is credit history (15%), or the length of time you’ve had your open credit cards and loans. Longer credit history will boost your score, while a bunch of new accounts will hurt it.

It makes sense, then, that new credit (10%) also matters. A hard credit check (also called a credit inquiry, often done when you apply for a new loan or credit card) will hurt you here. So think carefully before you apply for new credit—it will (temporarily) hurt your score.

And finally, there’s your credit mix (10%). If you have several different kinds of credit (think a mortgage, an auto loan, or some credit cards), you’ll have a higher score than if you just have one type of credit.

Personal loans and your credit

When you first submit a loan application, expect your personal credit score to take a hit. That’s because your lender will probably do a hard credit check, which―as you recall―negatively affects the new credit portion of your score.

Once you get approved and actually take out the loan, the new credit account may ding your credit history a bit. So while a personal loan may improve your credit mix (depending on what else you have), you shouldn’t be surprised if you see an overall (small) drop.

It gets better from there though. As you make payments over the course of your repayment term, you’ll improve your payment history and the length of your credit history―both things that can help your credit score. Unless, of course, you miss payments, which will hurt your payment history.

And if you decide to refinance your loan for debt consolidation, you may improve your amount owed if you use your new loan to pay off credit card debts. Yes, the new debt consolidation loan might mean a hit to your new credit―but that counts for less than your amount owed.

Altogether, your personal loan should have a net positive effect on your FICO credit score (as long as you keep up with loan payments, that is). Of course, you shouldn’t expect excellent credit overnight. But with some patience and time, your credit rating should improve.

Other ways to build your credit

Now you’ve seen that, yes, a personal loan can build your credit (though that may not happen right away). But personal loans are just one of the ways you can build credit.

For example, you can consider taking out one or more of the following types of credit:

- Home mortgage

- Auto loan

- Business or personal credit card

- Business loan or line of credit

- Student loan

- Other loans

These all have the potential to help your credit score―if you make regular on-time payments.

The takeaway

A personal loan won’t be a magic solution to a bad credit score. In fact, when you first get one, your personal credit score might drop a bit. But with each loan payment, you’ll work toward better credit. And in the end, you should find that your personal loan has helped build your personal credit.

So while we don’t advise you to take out a personal loan just to boost your credit (there are plenty of other things that can help with that), you don’t have to worry about a personal loan damaging your credit forever.

Good luck with your loan―and with building good credit!

Now that you’ve learned one way to build personal credit, learn more about how to build business credit.

Related content

Disclaimer

At Business.org, our research is meant to offer general product and service recommendations. We don't guarantee that our suggestions will work best for each individual or business, so consider your unique needs when choosing products and services.

Recent Articles

6Lendio vs. LendingTree Loans 2026

Which loan marketplace is better―Lendio or LendingTree? Business.org breaks down their pros and cons to...

LendingTree Loan Review 2026

Thinking about getting a business loan through LendingTree? Business.org explains how it works, what makes...

Lendio Review 2026: A Funding Marketplace to Save You Time and Money

We analyzed each of Lendio’s 10 business loan options to bring you our take on...

Best Small Business Loans

We researched more than 60 online and traditional lenders to come up with our list...